Software Isn't Dying, It's Consolidating

What the AI bear case gets wrong about enterprise HR tech, and why the real story is platform consolidation. Public market data as of 3/9/2026.

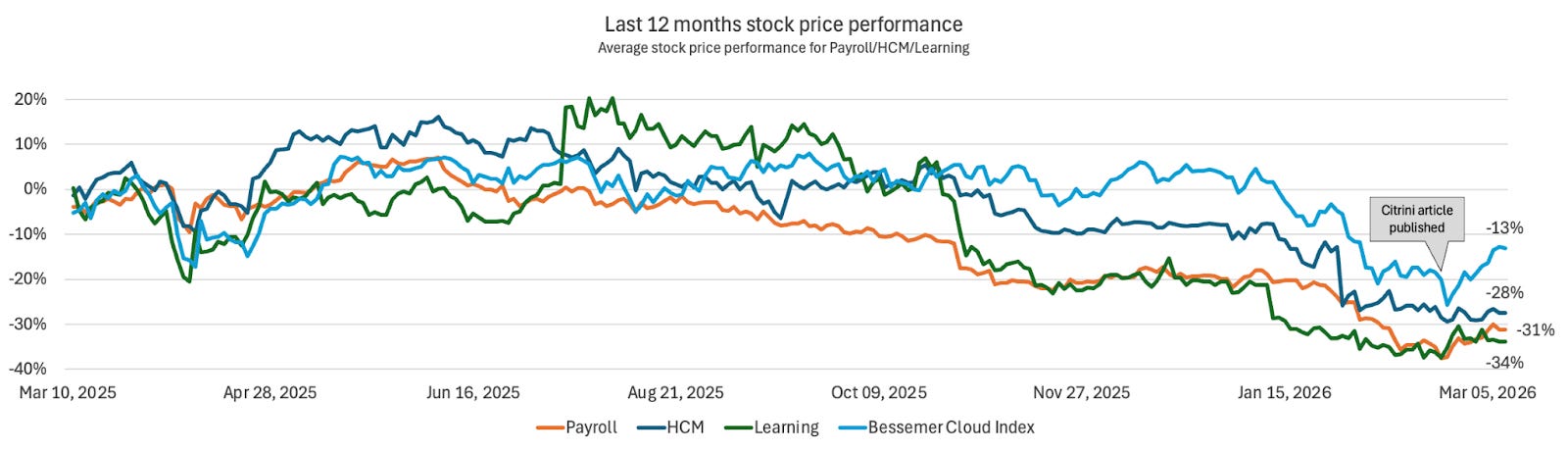

It’s been almost 4 weeks since Citrini Research’s article on the future of software went viral. Written as a theoretical perspective from 2028, the dystopian article outlines how AI could create an employment crisis where better AI capabilities lead to fewer workers needed and a spike in unemployment.

Software was already going through a selloff period on fears of AI disruption, and Citrini’s article perfectly described software’s bear case, triggering a sharp drop in stock prices. What happened next was a flood of responses from financial institutions, investors, tech executives, and really anyone with an X account. While the Citrini-triggered selloff has passed and the Bessemer Cloud Index has rebounded, the debate continues: Is generative AI good or bad for the software industry?

There are thoughtful people on both sides, and predicting the future of software is genuinely hard right now. Still, the fundamental premise of software hasn’t changed: One large team building a product for thousands of customers creates scale advantages in engineering, support, and reliability that no individual company can replicate internally. What’s changing is how software is being developed and how it is being paid for. To better understand the value proposition of enterprise software, you have to understand how enterprises actually buy software.

What enterprises want

When I talk to enterprise leaders, three things come up over and over again:

They want safe software that works: No errors or hallucinations, hard to breach, full audit logs, regulatory compliance, and the ability to clear procurement.

They want as few systems as possible: The less systems to manage, the better. Decent features from a core platform have an edge over best-of-breed solutions. There are hundreds of great examples, but Microsoft Teams versus Slack is one of the more well-known.

Switching software is an organizational transformation, not a technology swap: Replacing a CRM or HCM at a large company is a multi-year effort that touches workflows, reporting, compliance, training, and change management. Workday built a large part of its go-to-market on consulting partners running full workforce transformation projects alongside the software, and channel partners accounted for 25% of their net-new ACV last year.

These aren’t preferences that change because AI gets better. They’re structural features of how large organizations operate. And they create a gravitational pull toward the core platform.

The gravity of core platforms

That gravitational pull is what makes core platforms so durable. Over time, they become the center of their customer’s software galaxy, where point solutions revolve around and integrate with them. Every sales tool needs to integrate with Salesforce. Every HR tool needs to connect to Workday. And if Salesforce or Workday builds something similar to what a point solution offers, they’re the likely winner because they already have the trust, the data, and the integration surface area. A vendor that can’t integrate with the core platform has little chance of commanding a meaningful ACV, and that’s if they can even sell into the enterprise.

The scale economy logic of software (one team, thousands of customers) doesn’t just apply to the vendors themselves. It also explains why enterprises consolidate around a small number of platforms. Managing fewer vendors means less integration overhead, less security exposure, and less organizational change. The same instinct that makes SaaS economics work for the vendor also makes platform consolidation attractive for the buyer.

How generative AI accelerates consolidation

Generative AI accelerates this dynamic. Core platforms can now build and ship adjacent capabilities faster than ever before, consolidating solutions that previously required standalone vendors. The engineering leverage AI provides disproportionately benefits platforms that have data, distribution, and customer trust.

The counterargument is that AI-native platforms will offer a large enough improvement to justify the pain of switching. By automating time-intensive data entry workflows and repetitive tasks, these new systems of action are positioned to create and capture much more value than incumbents. If that promise is realized at scale, the switching calculus could shift in ways it hasn’t before.

Still, it’s worth remembering that organizational change takes time. When an enterprise adopts a new system of record, they’re typically making a 10+ year commitment. That decision involves years of evaluation, implementation, and organizational change before the new system is even fully operational. The technology being better isn’t enough on its own. The improvement has to be dramatic enough to justify a multi-year transition, and the vendor has to be trustworthy enough to bet the next decade on. That’s a bar that most companies, no matter how good their product is, will struggle to clear. The consolidation will happen, but it’ll happen on long timelines. Anthropic and OpenAI use Workday for a reason.

Narrowing to HR software

With that framework in mind, let me narrow the lens to the category I spend the most time in: HR SaaS. The same dynamics apply here, but with a few sector-specific wrinkles worth calling out.

The seat-based model is showing cracks. HR SaaS has always been tied to employee headcount and payroll volume, and for years that felt like a tailwind. But headcount growth has stalled across most segments, and enterprises are getting more cost-conscious about per-seat pricing. When customers are investing in AI to do more with fewer people, a pricing model that scales with headcount starts working against you. The revenue base isn’t collapsing, but the model that got these companies here may not be the model that takes them forward.

Payroll will get vibe-implemented, but not vibe-coded: Just as Stripe simplified payments, I expect payroll implementation to get dramatically easier over time. However, the core payroll engine that handles complex infrastructure (constantly changing tax codes, live connections to authorities, garnishments, and benefits) won’t be commoditized by AI coding tools, even if the abstraction layer changes.

AI in hiring is running into regulatory and legal walls: Workday and Eightfold both face lawsuits that challenge their status as neutral tool providers. Workday is accused of discrimination via its AI screening, with the court finding it acted as an employer’s agent, triggering direct liability. Eightfold faces a proposed class action for building candidate reports with scraped data, allegedly violating the Fair Credit Reporting Act (FCRA). Regardless of where the cases land, they are starting a necessary conversation about disclosures to candidates and how much autonomy in hiring decisions AI should have. The legal framework hasn’t caught up to the technology, and widespread adoption of these tools will likely wait for answers.

The bottom line

Enterprise software isn’t dying, it’s transforming. The scale advantages of building one product for thousands of customers are arguably more real today than ever. Enterprises are and will remain cautious buyers who want safe, compliant, and integrated systems.

Still, durable demand doesn’t mean that incumbents will gracefully navigate this technology shift. Companies that are built on seat-based pricing are watching their customers invest in doing more with fewer people, and that creates real counter-positioning risk. Seat-based revenue is still enormously profitable, which makes it hard for incumbents to voluntarily cannibalize it by moving toward consumption or outcome-based models. Workday’s “Consumption Flex” credits and Docebo’s usage-based pricing experiments are early signs the industry sees the shift coming, but these are incremental moves from companies protecting large installed bases. A challenger with no legacy revenue to protect can build around the new pricing architecture from day one. The longer incumbents wait to make that transition, the wider the window gets for someone else to own it.

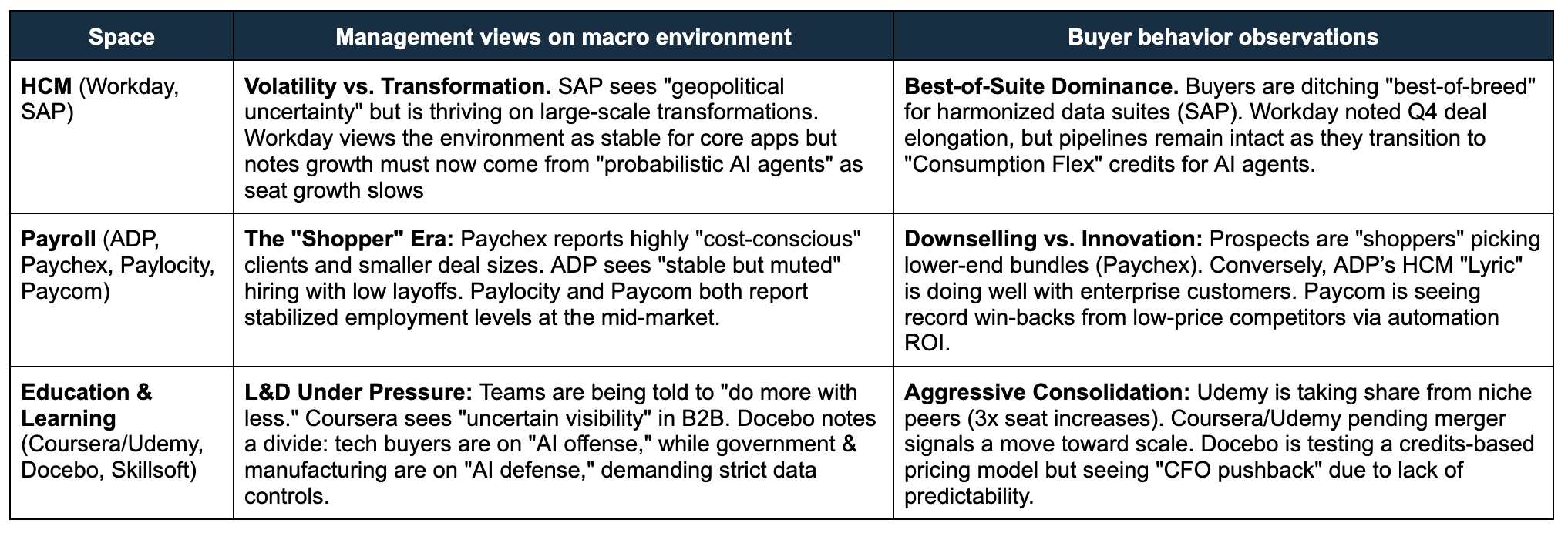

Quarterly HR SaaS “vibe check”

The table below translates the consolidation thesis into what’s actually showing up in public company earnings. A volatile macro environment is elongating sales cycles and tightening budgets. Customers are cost-conscious and only appear willing to pay up for AI agents that provide real automation. AI adoption is creating new pricing models but CFOs are cautious to commit to less predictable expenses.

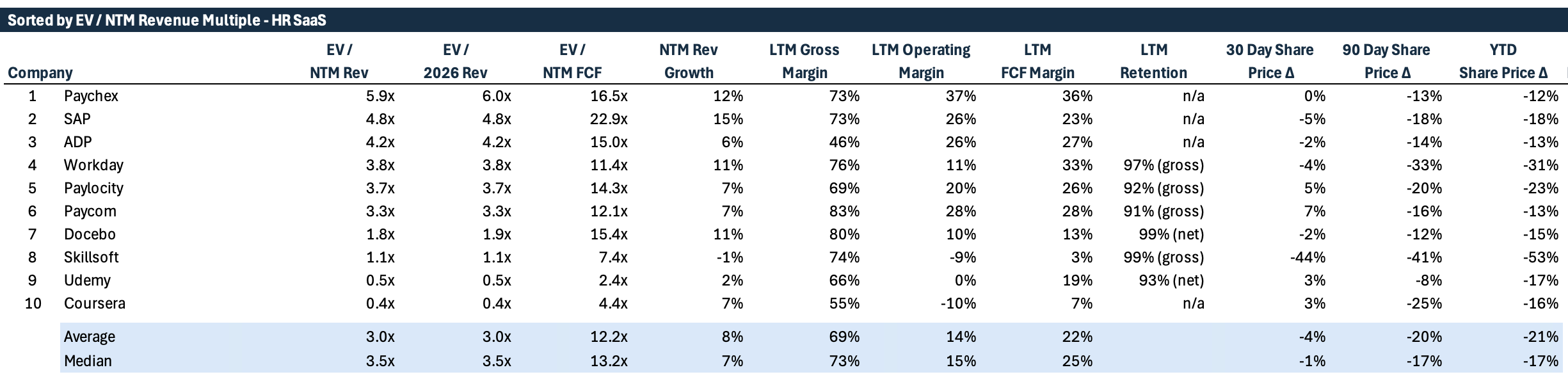

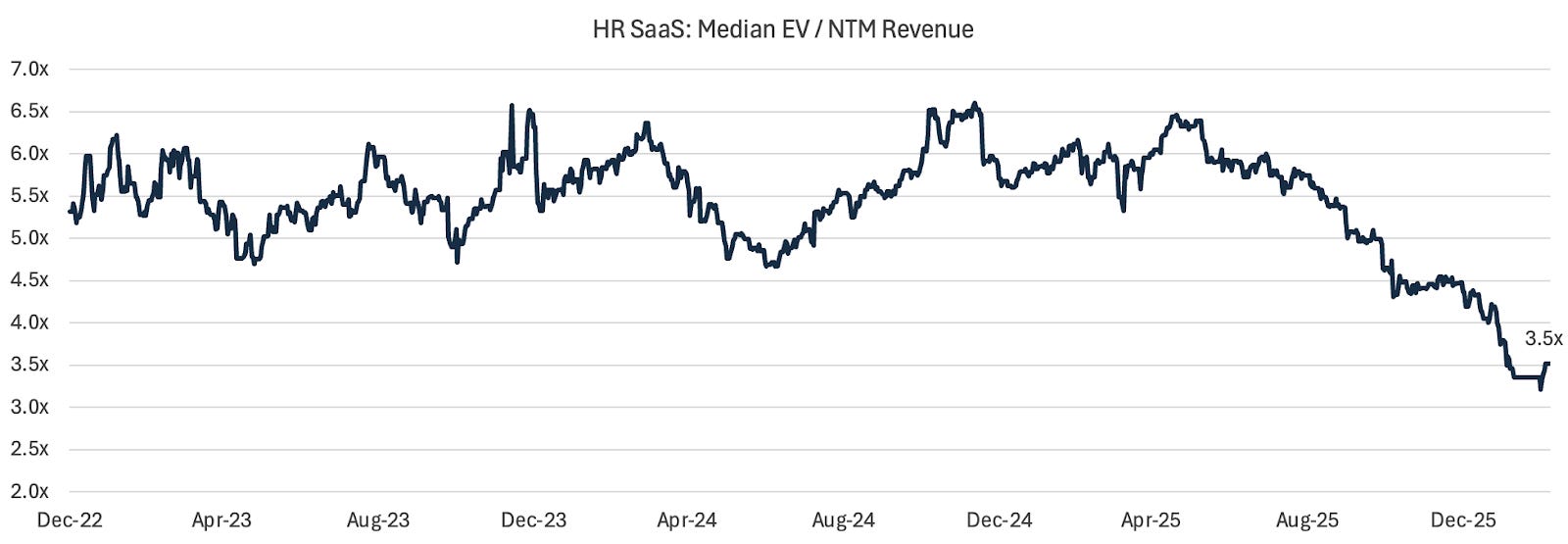

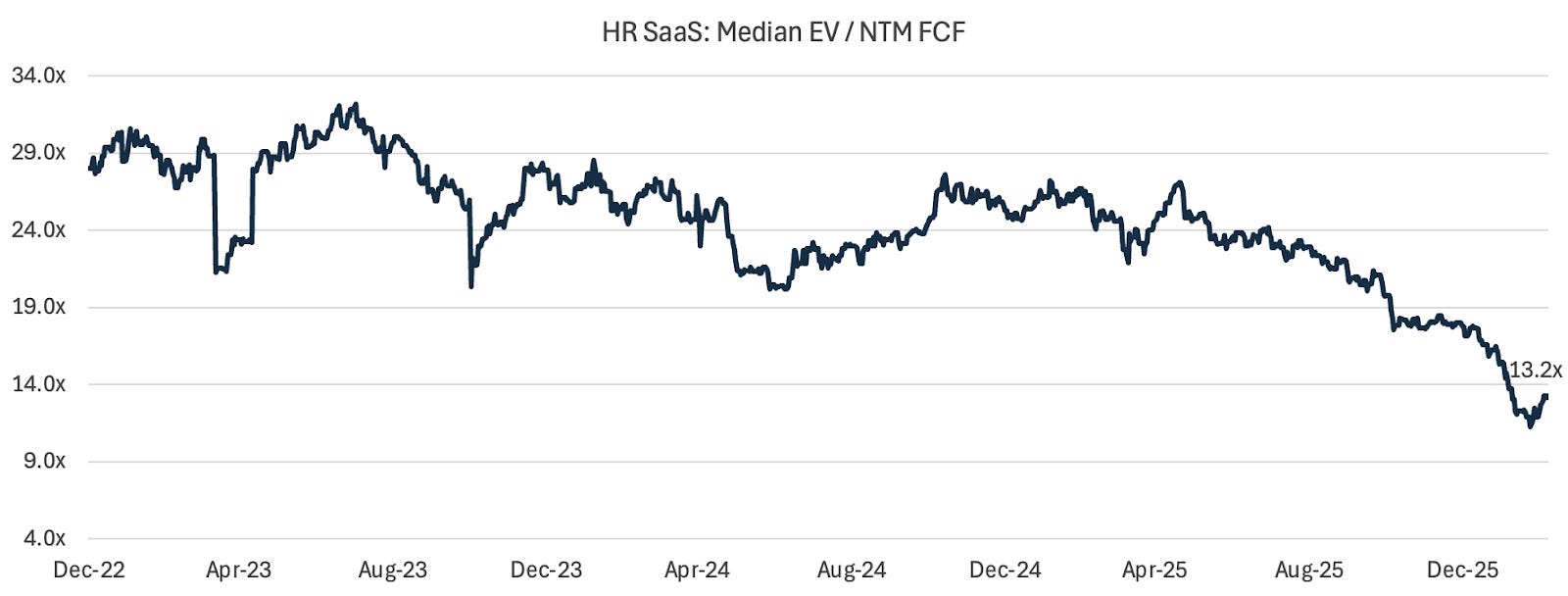

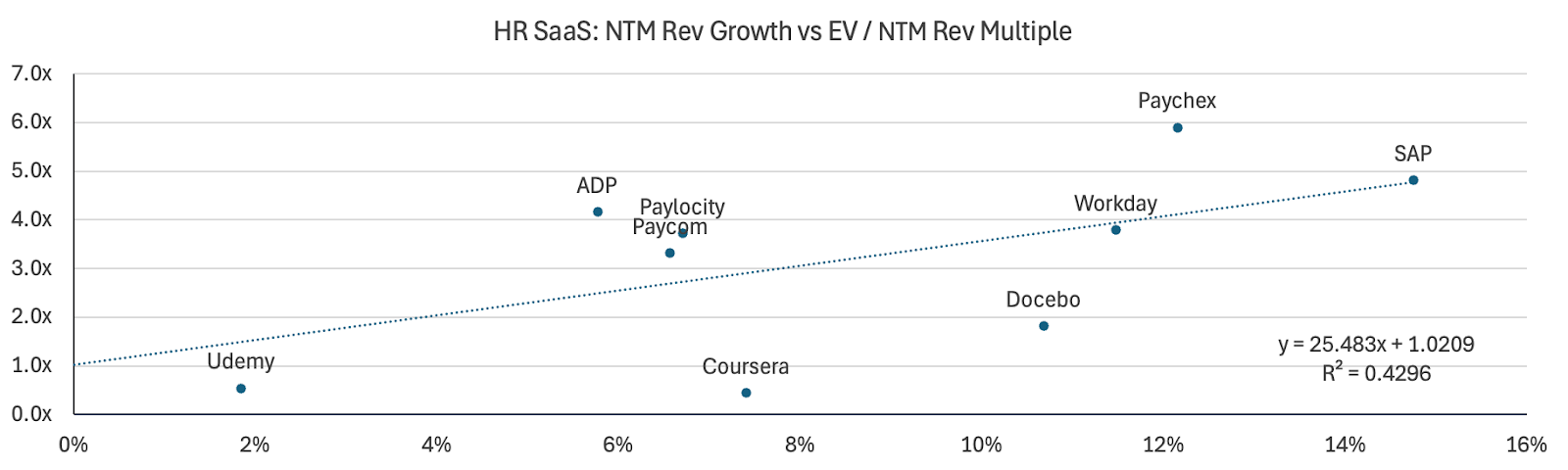

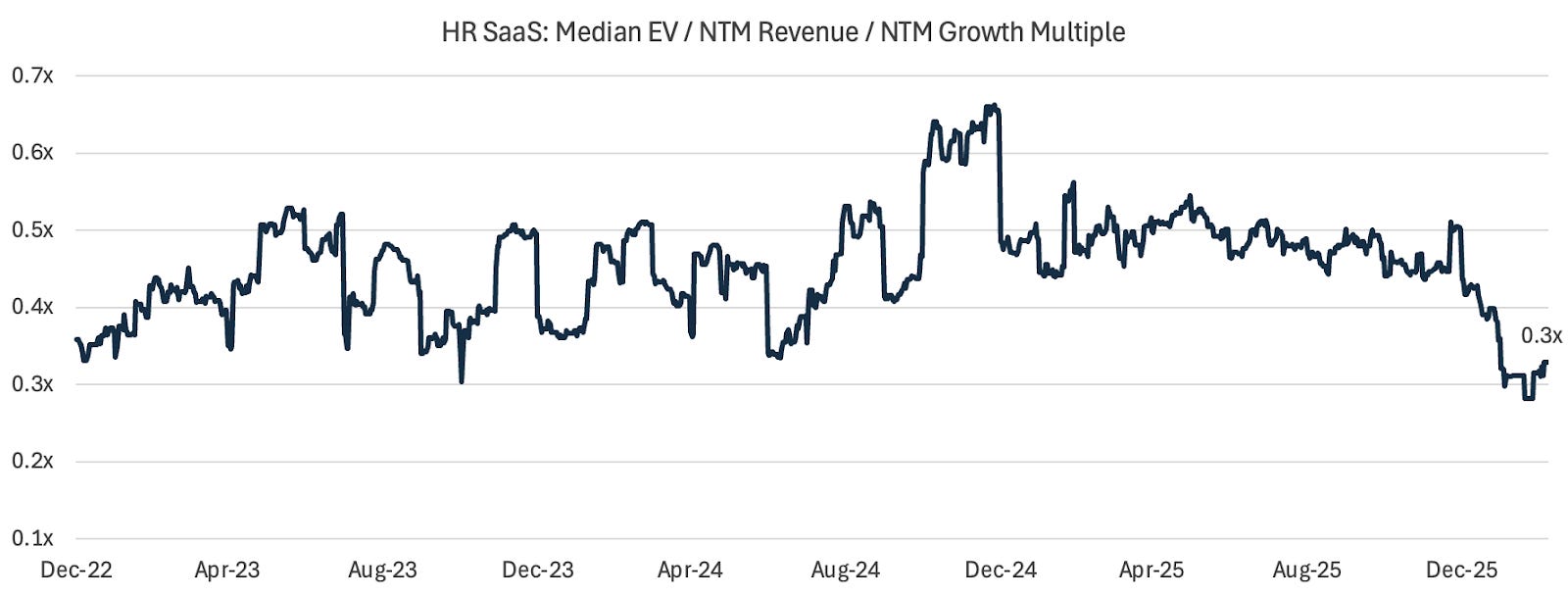

Charts and graphs

If you’re an operator or investor in the space, I’d love to hear from you. Please reach out at kgetsiv@indeed.com

Thanks for reading!

Footnotes & Disclosures:

The information presented in this publication is for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. The views expressed are solely those of the author and do not represent the views of any company, employer, or affiliated party.

All data and analysis are derived from public sources, including Pitchbook and company websites. No confidential or proprietary information has been used or referenced. While the information is believed to be accurate and from reliable sources, no warranty is made as to its completeness or accuracy, and no liability is accepted for errors or omissions. Past performance is not indicative of future results.